FHN Financial Economic Weekly: Friday, December 12, 2025

A Dovish Cut After All

Wednesday's FOMC vote to cut rates was close, but communication was more dovish than expected. There were two formal dissents against a cut, and another four of 19 committee members wanted to leave rates unchanged. There is no way to know — yet — how many of these were voters, but we will soon now that the communication blackout is over.1 The dot plot median still points to just one cut next year. Still, we expect the Fed will cut three times next year as inflation slows and the job market continues to sputter. As Chair Jay Powell told reporters, no one on the FOMC believes the next move is a hike. Disagreement among committee members is not whether to hike or cut, it's when to cut next.

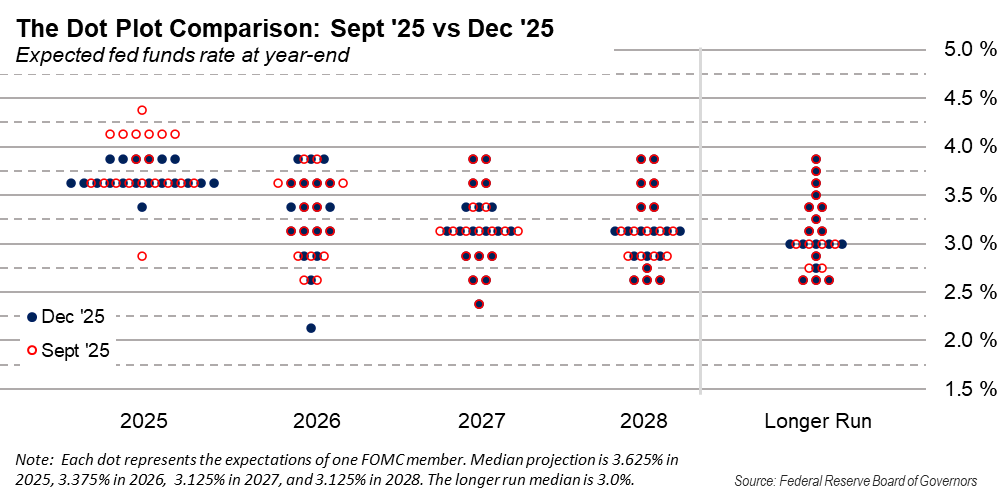

Reading the dot plot

The dots in the new dot plot moved very little, but movement was mostly upward. The 2026 dots gravitated toward the center. One dot in 2027 is higher, another moved higher in '28, and one long-run dot was also higher in December than in September. Not much of a change, but a change nonetheless.

1 While it sounds odd that a voter would vote against a policy decision without formally dissenting, there is ample precedent, usually because a participant does not want to pile on or did not feel strongly.

The median neutral rate estimate is 3%, but the range of estimates is still very wide, from just above 2.5% to just below 4%. The central tendency stretches from 2.75%-3.5%. The dispersion of long-run neutral-rate estimates explains most of the dispersion of estimates over the next three years. As Powell mentioned in the press conference, with the cut this week, the target rate is now within the range of estimates of neutral. The range, however, is broad. The committee will find neutral by watching data as it comes in. If the inflation rate keeps falling, neutral is lower. If it stabilizes, the implication is we are there already.

Near agreement

As noted in prior weeklies, Fed hawks and doves are closer in thinking than you might think. Chair Powell made that clear in the press conference, when he noted all participants are worried about inflation and all are worried about the labor market. Their policy differences stem from how they assess these risks. A quick review

The hawks are primarily focused on inflation risk. As Governor Michael Barr recently noted, inflation from tariffs is both structural and transitory, but so was the inflation after the pandemic lockdowns. Nevertheless, inflation has been elevated since 2021. After four years of above target inflation, Barr worries it could become embedded in expectations. Jeff Schmid and Alberto Musalem share that fear. In effect, they are worried one-off structural inflation could become persistent cyclical inflation if it continues for much longer. Chicago Fed President Austan Goolsbee cited this specifically in his dissent explanation this morning.

The doves are primarily focused on the job market. San Francisco Fed President Mary Daly notes there is a structural problem limiting hiring — year to date immigration is deeply negative. DHS reports 1.6 million people have voluntarily self-deported and another 527,000 have been deported or are in detention centers awaiting deportation. Against that tide, approximately 20,000 people have entered the country illegally, mostly through Canada. But Daly notes that if weak job growth was mostly caused by a worker shortage, wages would be accelerating higher. Slowing wage growth is proof it is weak labor demand, and not supply, that is the predominant force. Chair Powell pointed out the same thing in his press conference, citing the third quarter employment cost index data released on the morning of the meeting.

The doves are also aware inflation has been above target for years, something Chris Waller, Miki Bowman, and Stephen Miran note the worst of tariff inflation has passed. The core PCE deflator fell from 2.9% to 2.8% in September. More important than the small, recent progress made, however, is the progress likely to come early next year without new tariffs adding new monthly inflation pressure.

The biggest core inflation increases this year were in January and February, suggesting companies jumped the gun and started raising prices when tariffs were threatened, rather than waiting for implementation. If inflation continues at its recent 0.2% monthly increase pace, core PCE inflation will be 2.46% year-on-year by the February release. The Fed is unlikely to cut rates in January, but a March cut is possible if inflation slows to less than 2.5%.

More cuts than let on if data cooperates

Based on the median in the new dot plot, the Fed is penciling in just one 25bp cut next year, and one more in 2027. The December dot plot will not determine policy next year, however, as it is just a point-in-time projection. Policy will be determined by the data, because the data will reveal whose forecasts are on target and whose are off the mark. As Powell noted on Wednesday:

"Interestingly, everyone around the table at the FOMC agrees that inflation is too high and we want it to come down and agrees that the labor market has softened and that there is further risk. Everyone agrees on that. "Where the difference is, is how do you weight those risks and what does your forecast look like and where do — ultimately — where do you think the bigger risk is? And, you know, it's very unusual to have persistent tension between the two parts of the mandate. And, when you do, this is what you see. And I think it's actually what you would expect to see. And we do see it." |

The tension between the inflation and employment mandates reflects structural change introduced by the tariffs. Inflation would have dropped year-to-date if import costs had not jumped early this year. Cyclically, the economy is restrained thanks to three-and-a-half years of restrictive Fed policy. Looking forward, inflation will slow because the President has stopped imposing new tariffs and has shifted to fine tuning existing ones. Their impact will pass from inflation and cyclical factors will take control. When they do, the Fed will be ready to act. As Powell went on to say:

"Meanwhile, the discussions we have are as good as any we've had in my 14 years at the Fed. They're very thoughtful, respectful. And you just have people who have strong views. And, you know, we come together and we reach, you know, a place where we can make a decision. We made a decision today. We had — you know, nine out of 12 supported it. So fairly broad support. But it's not like the normal situation where everyone agrees on the direction and what to do. It's more spread out. And I think that's only inherent in the situation. "In terms of what it would take, you know, we all have an outlook in terms of what's going to come, but I think, ultimately, having cut 75 and, you know, the effects of the 75 basis points will only begin to be coming in, as I've said before a couple times, we're well positioned to wait to see how the economy evolves. We'll just have to see. And we will get, as you know, quite a bit of data." |

All but one or two of the 19 on the FOMC believes the Fed is done easing. When Nick Timiraos asked, given the change in language in the statement, if the next move could just as easily be a hike as a cut, Powell told him no. No one on the FOMC is talking about rate hikes.

Add the fact hawks and doves agree tariffs cause only transitory inflation — a recent San Francisco Fed paper on 150 years of tariff policy found tariffs cause higher unemployment and lower inflation even in the short run — resistance to rate cuts is likely to fade as soon as inflation starts to drop. The policy pause reflects the difference of opinion over how long that will take.

Powell acknowledges productivity

As we wrote last week, productivity is another critical factor affecting next year's rate outlook. CNBC's Steve Liesman, in a discussion about the Fed's new forecast, noted, "You've got a big increase in the growth numbers, but not a big decline in the unemployment numbers. Is that an AI factor in there?"

Powell agreed, and it's more than AI. "The implication is obviously higher productivity. Some of that might be AI, but also, I think productivity has just been, almost structurally, higher for several years now. So, if you start thinking of it as 2% per year, you can sustain higher growth without more job creation. Of course, productivity is also what enables incomes to rise over periods of time, so it's basically a good thing, but that's certainly the implication."

Rapid productivity growth not only allows stronger economic growth, it demands stronger economic growth. If productivity is a percentage point or two faster than normal, GDP growth also must be a percentage point or two faster than normal to maintain normal job growth.

This week's labor data confirm labor weakness

It will be months before government data catches up with its normal release calendar. We're still getting third quarter releases. Powell noted there will be no October household employment data and the Fed will read the November data with a skeptical eye. Meanwhile, we learned a few new things about labor market conditions from two releases this week. First, the JOLTS report, which showed a widening labor mismatch, supporting the hawkish view.

Job openings unexpectedly rose from 7.227m in August to 7.658m in September and 7.670m in October. At the same time, the quit rate fell from 2.0% in September to 1.8% in October, the lowest since the pandemic lockdowns. Quits normally rise along with opportunity. The combination of significantly higher openings and a lower quit rate suggests there are plenty of jobs, but not in fields interesting to job seekers. The increase in openings could well reflect the loss of immigrant, unskilled labor, while the low quit rate suggests people are holding onto entry-level jobs usually freed up for new, highly-trained workers entering the job market.

On the flip side, the employment cost index rose just 0.8% in the third quarter. Slower compensation growth indicates companies are not scrambling for workers. If they were, they would pay up. As with all things economic, when there is uncertainty about supply and demand, the intersection of the two — price — indicates which has the upper hand. Wages are the price of labor. Slower wage growth supports the contention labor demand is weakening faster than labor supply.

The fog of uncertainty posed by productivity — it is strong, but how strong? — immigration policy, still-uncertain 2026 fiscal policy, and disagreement over the level of neutral fed funds means the Fed will monitor progress on inflation and employment to make rate decisions next year. As data rolls in, the dot plot will tighten around the participants with the most accurate forecasts. The Fed is paused now, but there are at least two more rate cuts coming. There could be as many as three. Their timing will depend primarily on inflation progress. For now, we are optimistic enough about 2026 inflation to go with cuts in March, June, and September.

– Chris Low, Chief Economist

The Week Ahead

Review and Preview

The Fed cut rates a quarter-point this week, but it was so well anticipated there was very little movement in market interest rates. Three- and 6-month Treasury bills moved most, falling 8bp since last Friday thanks to the surprise announcement by the Fed that it will buy T-bills to grow its balance sheet again, sooner than expected, to maintain its size relative to the economy. Further out the curve, 2-year notes are just 2bp lower and other coupons are up as much as 6bp, effectively a neutral reaction to a much-anticipated meeting.

There was not much data released this week. September and October JOLTS were published together. The biggest surprises were higher job openings and a lower quit rate. As noted in the main write-up, this combination suggests a growing jobs mismatch.

Still, the lower-than-expected 0.8% rise in the ECI suggests wage pressures are still receding, which in turn suggests labor-demand weakness outweighs labor-supply weakness.

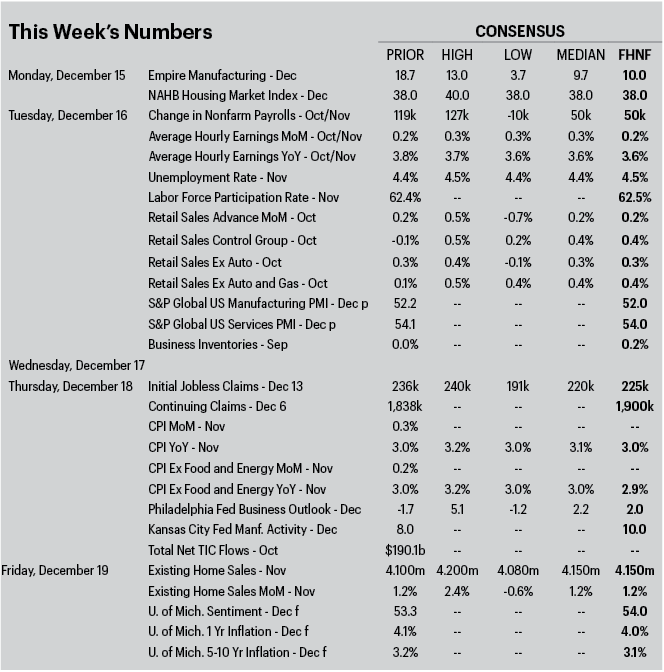

Next week's release calendar is quite busy.

Tuesday brings the November employment report, which will include October and November payrolls as well as the November household survey, including the November unemployment rate. We expect October payrolls fell 25k and November payrolls rose 50k. The October drop reflects federal government layoffs. October retail sales will also be released on Tuesday.

The November CPI release is on Thursday. There was no survey in October, so there will be no monthly changes reported. The BLS may report average October/November monthly changes, however, and even if they do not, economists will calculate them. We expect headline and core averages of 0.2%.

There is a chance the headline CPI average monthly rise could round down to 0.1%, as gas prices fell in October and were up just a bit in November before plunging in December. Yesterday, the AAA national average price was $2.93. The price has been under $3.00 since November 30. The last time gas cost less than $3.00 a gallon was May 10, 2021, when it averaged $2.95 a gallon.

Today, Austan Goolsbee, who this week dissented against cutting rates, explained he wants to see more inflation data before supporting further rate cuts, adding he expects to support just one cut next year. He is not a 2026 voter, however.

Jeff Schmid also dissented against this week's rate cut. In his dissent, he wrote, "Inflation remains too high, the economy shows continued momentum, and the labor market — though cooling — remains largely in balance. I view the current stance of monetary policy as being only modestly, if at all, restrictive. With this assessment, my preference was to leave the target range for the policy rate unchanged at this week's meeting."

Beth Hammack, who will vote next year, said she would have been happier with "slightly more restrictive rates," suggesting she was one of the six highest 2025 dots.

Next week, Stephen Miran, John Williams, Chris Waller, and Raphael Bostic have scheduled appearances.

– Chris Low, Chief Economist

News & Insights

Stay informed with the latest updates, market insights, and company news.